STRATEGY INDEX

- Understanding the Opportunity: Why Black-Scholes Still Matters

- The Core Inputs: Deconstructing the Black-Scholes Formula

- Practical Implementation Blueprint: From Theory to Trade

- Leveraging Volatility Insights: The Engine of Option Pricing

- Risk Management Protocol: Navigating the Options Landscape

- The Quant Guild Advantage: Tools and Resources for the Aspiring Quant

- Executing Your Strategy: The Brokerage and Tech Stack

- Strategist's Verdict: Is Black-Scholes Your Next Profit Center?

The world of financial markets is in constant flux, yet some foundational principles remain remarkably robust. Among these, the Black-Scholes model stands as a cornerstone for understanding and pricing options. While often perceived as a theoretical construct, its practical application is a critical skill for any trader aiming to gain a quantitative edge. This guide isn't about abstract formulas; it's about transforming that theory into actionable trading strategies that can potentially unlock significant returns. We will dissect the model, explore its critical inputs, and provide a clear roadmap for its implementation, turning complex calculations into a profitable trading arsenal.

Understanding the Opportunity: Why Black-Scholes Still Matters

In today's fast-evolving financial landscape, the ability to accurately price and strategize around options is paramount. The Black-Scholes model, despite its age, remains a powerful tool for quantitative analysts and traders. It provides a standardized framework to estimate the theoretical value of European options, essential for identifying potential mispricings in the market. Mastering this model is akin to acquiring a secret decoder ring for option premiums, allowing you to move beyond guesswork and into informed decision-making. This is not merely about calculating prices; it's about understanding the sensitivity of those prices to various market factors – a crucial differentiator for generating alpha.

The opportunity lies in the discrepancies that can arise between theoretical values and market prices. By understanding the Black-Scholes framework, you can identify when an option might be overvalued or undervalued, creating a strategic advantage. Furthermore, the model's components, particularly implied volatility, offer profound insights into market sentiment and expected future price movements. This knowledge is invaluable for developing sophisticated trading strategies, from simple directional bets to complex multi-leg options plays. For serious traders looking to elevate their game, incorporating this model is a non-negotiable step towards optimizing their investment portfolios and maximizing their ROI.

To truly grasp the power of this model, consider its implications for portfolio construction. A well-understood options strategy can offer protection against downside risk or provide leverage to capitalize on anticipated market moves. This dual functionality makes it an indispensable tool for sophisticated investors aiming for both growth and capital preservation. As quantitative finance continues to dominate market strategies, the Black-Scholes model remains a foundational element, attracting significant attention from academic institutions and hedge funds alike, underscoring its enduring relevance.

The Core Inputs: Deconstructing the Black-Scholes Formula

The elegance of the Black-Scholes model lies in its simplicity, relying on five key inputs to derive a theoretical option price. Understanding each of these is fundamental to its successful application:

- Current Stock Price (S0): This is the current market price of the underlying asset. It's the most dynamic input and forms the baseline for valuation.

- Strike Price (K): The price at which the option holder can buy or sell the underlying asset. This is predetermined and fixed at the time the option is created.

- Time to Expiration (T): The remaining lifespan of the option, typically expressed in years. The longer the time until expiration, the more value an option generally holds due to increased potential for favorable price movements.

- Risk-Free Interest Rate (r): This represents the theoretical return of an investment with zero risk, usually approximated by government bond yields. It accounts for the time value of money.

- Volatility (σ): Perhaps the most critical and challenging input, volatility measures the expected fluctuation of the underlying asset's price. Higher volatility generally leads to higher option premiums, as the probability of significant price swings increases.

"The Black-Scholes model is a beautiful piece of financial engineering. But like any tool, its effectiveness depends entirely on the quality of the inputs and the skill of the operator." - The Financial Strategist

Accurately estimating volatility is where much of the complexity and opportunity lies. Often, analysts use implied volatility derived from current market option prices, or historical volatility calculated from past price data. The choice between these inputs can significantly impact the model's output and, consequently, your trading decisions. For traders looking to refine their edge, understanding the nuances of volatility forecasting and its impact on option premiums is a critical area of study. This is where the real arbitrage opportunities can be found, moving beyond simple price calculations to strategic market positioning.

Mastering the sensitivity of the option price to each of these variables, known as the 'Greeks' (Delta, Gamma, Theta, Vega, Rho), is the next logical step. For instance, Vega directly measures an option's sensitivity to changes in volatility, making it a vital metric for strategies that aim to profit from shifts in market expectations. Understanding these relationships allows for more nuanced trading strategies, potentially mitigating risk and enhancing reward.

Practical Implementation Blueprint: From Theory to Trade

Translating the Black-Scholes model from theoretical equations to a live trading strategy requires a structured approach. This blueprint outlines the essential steps to move from understanding the formula to actively trading options:

Phase 1: Foundational Knowledge Acquisition

- Master European Options: Before diving into Black-Scholes, ensure a solid grasp of European options, their characteristics, and how they differ from American options. This foundational knowledge is crucial for understanding the model's limitations and applications. Learn the basics of European Options.

- Understand the Black-Scholes Equation: Dedicate time to understanding the mathematical derivation of the Black-Scholes formula. While you may not need to derive it daily, conceptual understanding empowers you to troubleshoot and adapt the model. Explore the derivation process.

- Grasp the 'Greeks': Familiarize yourself with the sensitivities of option prices (Delta, Gamma, Theta, Vega, Rho). These are derived from the Black-Scholes model and are essential for risk management and strategy development.

Phase 2: Data Acquisition and Tools Setup

- Secure Reliable Data Feeds: Access to real-time or historical data for the underlying asset price, strike prices, interest rates, and crucially, implied volatility is vital. Many brokerage platforms and financial data providers offer this.

- Choose Your Implementation Method:

- Spreadsheet Software (e.g., Excel, Google Sheets): Suitable for simpler calculations and learning. Many pre-built templates are available, or you can build your own.

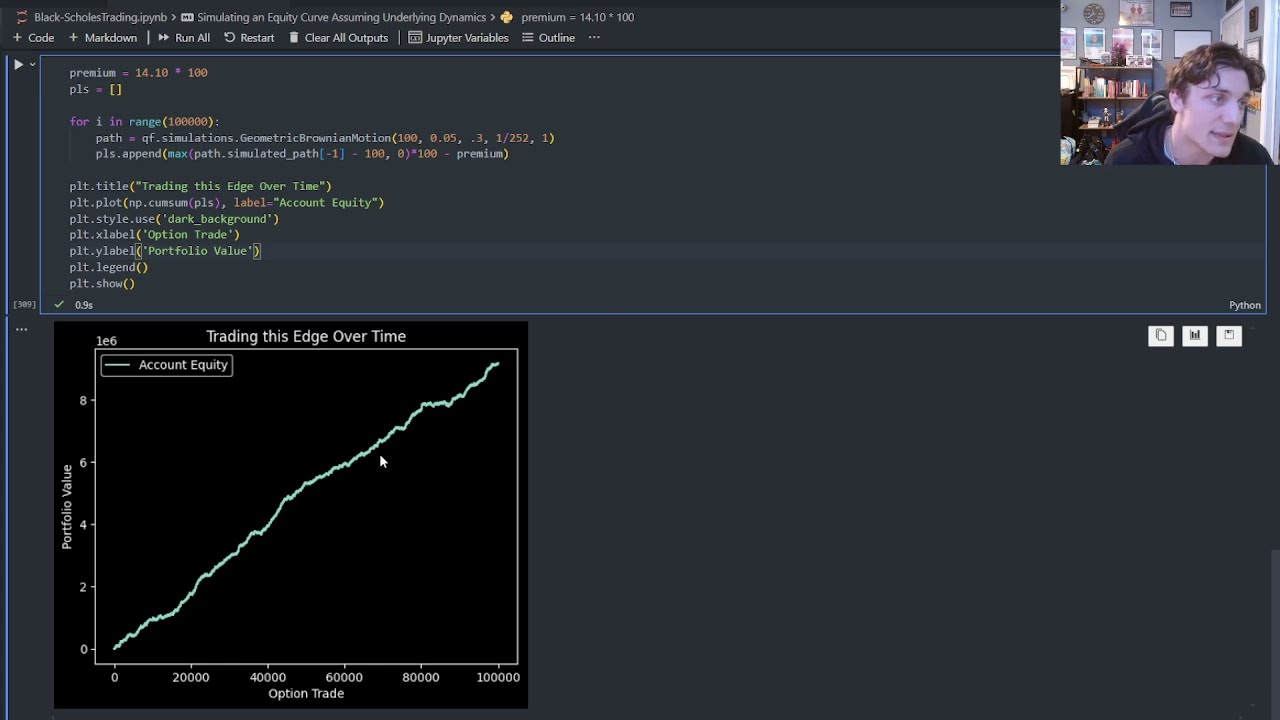

- Programming Languages (e.g., Python): Offers the most flexibility for complex strategies, backtesting, and automation. Consider libraries like NumPy and SciPy. A practical example can be found in this Jupyter Notebook.

- Financial Software Packages: Many professional trading platforms include integrated option pricing tools.

- Select a Brokerage Account: Choose a reputable broker that offers options trading and the tools or APIs you need for implementation. Interactive Brokers is a popular choice for algorithmic traders due to its advanced platform and extensive market access.

Phase 3: Strategy Development and Testing

- Calculate Theoretical Prices: Use your chosen implementation method to calculate the theoretical value of options for a given asset.

- Compare with Market Prices: Monitor live market prices and identify discrepancies between market premiums and your theoretical calculations.

- Develop Trading Rules: Based on your analysis, define clear rules for entering and exiting trades. For example, "If the market price is X% higher than the Black-Scholes value, consider selling the option."

- Backtest Your Strategy: Before risking real capital, test your trading rules on historical data to evaluate their past performance and potential profitability.

Phase 4: Live Trading and Optimization

- Execute Trades: Start with small position sizes to gain experience in a live environment.

- Monitor and Manage Risk: Continuously track your positions, re-evaluate model inputs, and manage your 'Greeks' to control risk exposure.

- Iterate and Refine: Market conditions change, and so should your strategy. Regularly review your performance, adjust your parameters, and update your model as needed.

This structured approach ensures that you are not just calculating numbers but are building a robust trading system based on sound financial principles. Remember, consistency and disciplined execution are key to long-term success in options trading.

Leveraging Volatility Insights: The Engine of Option Pricing

Volatility is the lifeblood of options trading. The Black-Scholes model inherently recognizes this, making implied volatility (IV) a crucial determinant of an option's price. Understanding and effectively leveraging IV is not just about plugging a number into a formula; it's about interpreting market sentiment and forecasting future price potential.

Implied volatility represents the market's consensus expectation of an asset's future price swings over the life of the option. Unlike historical volatility, which looks backward, IV is forward-looking. It's derived directly from the prices of options trading in the market. When market participants anticipate significant price movements (due to news, earnings, or economic events), demand for options increases, pushing up their prices and, consequently, their implied volatility. Conversely, periods of calm and low expected price movement lead to lower IV.

Market Implied Volatility is a key driver for option traders. A trader might sell options when IV is perceived as high, betting that actual realized volatility will be lower than implied. Conversely, buying options when IV is low assumes that future volatility will increase. This 'volatility trading' is a sophisticated strategy that leverages the Black-Scholes model's sensitivity to IV (Vega) to profit from changes in market expectations. For instance, if you believe the market is overestimating future volatility for a particular stock, you might sell call and put options to profit from the premium decay and the potential drop in IV. Conversely, if you anticipate a significant event that will cause sharp price movements, buying options when IV is relatively subdued could offer considerable leverage.

The VIX index, often referred to as the "fear index," is a prime example of how volatility is centrally tracked and traded. While the VIX tracks the implied volatility of the S&P 500 index options, similar principles apply to individual stocks. Analyzing the IV skew and term structure can further refine trading strategies. The IV skew refers to how IV differs across various strike prices for options with the same expiration date. Typically, out-of-the-money (OTM) puts have higher IV than OTM calls, reflecting a higher market demand for downside protection. The term structure shows how IV varies with expiration dates. Understanding these nuances allows traders to select options contracts that align with their volatility outlook and risk tolerance, making IV analysis a cornerstone of advanced options trading.

Risk Management Protocol: Navigating the Options Landscape

Successfully trading options using the Black-Scholes model necessitates a robust risk management protocol. The leverage inherent in options trading amplifies both potential profits and losses, making disciplined risk management not just advisable, but critical for survival.

The Financial Strategist is a business consultant and market analyst with over a decade of experience helping entrepreneurs and investors maximize their profitability. Their approach is data-driven, systematic, and focused on ruthless execution.

1. Understand and Monitor the 'Greeks': As discussed, the Greeks (Delta, Gamma, Theta, Vega, Rho) are indispensable tools for measuring and managing portfolio risk.

- Delta: Measures the sensitivity of the option price to a $1 change in the underlying asset's price. A delta-neutral strategy aims to profit from factors other than price direction.

- Gamma: Measures the rate of change of Delta. High Gamma means Delta changes rapidly, indicating higher risk in volatile markets.

- Theta: Measures the rate of time decay. Options lose value as expiration approaches, and Theta quantifies this daily erosion.

- Vega: Measures sensitivity to changes in implied volatility. Crucial for strategies betting on volatility shifts.

- Rho: Measures sensitivity to changes in interest rates. Generally less significant for short-dated options.

Regularly calculating and monitoring your portfolio's aggregate Greek exposures allows you to identify and hedge unwanted risks. For instance, if your portfolio's Delta becomes too high, indicating significant exposure to upward asset price movements, you might hedge by selling futures or buying put options.

2. Position Sizing: Never risk an amount that would jeopardize your overall financial health. A common guideline is to risk no more than 1-2% of your trading capital on any single trade. For options, this means carefully calculating the premium paid or the potential margin required.

3. Diversification (Within Constraints): While concentrated bets can yield high returns, they also carry high risk. Diversify your option strategies across different underlying assets, expiration dates, and volatility profiles. However, be mindful of over-diversification, which can dilute potential gains and make management complex. The goal is intelligent diversification that enhances risk-adjusted returns.

4. Stop-Loss Orders and Contingency Planning: Define exit points *before* entering a trade. Use stop-loss orders to automatically exit a position if it moves against you beyond a predetermined level. Have contingency plans for unexpected market events. What will you do if a major news event causes extreme volatility overnight? Having a plan in place prevents emotional decision-making during stressful market conditions.

5. Continuous Learning and Adaptation: The markets are dynamic. What worked yesterday might not work today. Regularly review your trading performance, identify weaknesses in your strategy, and update your risk management protocols. Consider resources like Quant Guild for continuous learning and skill enhancement.

"Risk your capital, not your financial future. The market always offers new opportunities; ensure you are there to take them." - The Financial Strategist

By implementing these risk management principles, you can navigate the complexities of options trading with greater confidence, turning potential pitfalls into calculated opportunities for growth. A well-defined risk management strategy is the bedrock of any sustainable trading operation.

The Quant Guild Advantage: Tools and Resources for the Aspiring Quant

For those serious about quantitative trading and complex financial modeling, access to the right resources and community can be a significant advantage. Quant Guild aims to provide a comprehensive ecosystem for quantitative finance professionals and aspiring quants.

This platform offers a wealth of educational materials, including detailed tutorials, coding libraries, and community support. A key resource for anyone looking to implement the Black-Scholes model is their extensive GitHub repository, which hosts practical code implementations and examples. For instance, the Jupyter Notebook on Black-Scholes Trading provides a hands-on approach, allowing you to run the model and explore its outputs directly. This practical, code-driven learning is invaluable for bridging the gap between theory and real-world application.

Furthermore, Quant Guild fosters a community aspect through its Discord server. Engaging with fellow quantitative traders and analysts offers a unique opportunity to discuss strategies, troubleshoot problems, and stay abreast of the latest market trends and analytical techniques. The collaborative environment is essential for refining models and developing robust trading systems. You can join the Quant Guild Discord server to become part of this dynamic network.

Beyond specific model implementations, Quant Guild's blog provides in-depth articles and code walkthroughs on various quantitative finance topics, accessible via their Medium publication and Roman Michael Paolucci's personal Medium page. These articles often delve into the practical applications of financial theories, offering insights that can directly inform trading strategies. For those who prefer direct code access, their GitHub profile and the broader Quant Guild GitHub house a variety of useful libraries and projects. By leveraging these resources, traders can significantly accelerate their learning curve and enhance their ability to develop and execute sophisticated quantitative trading strategies.

Executing Your Strategy: The Brokerage and Tech Stack

The theoretical prowess of the Black-Scholes model means little without the right infrastructure to execute trades and manage the underlying data. Building an effective technological stack is as critical as understanding the model itself. For quantitative traders, this typically involves a combination of a robust brokerage platform, reliable data sources, and potentially custom-built software or scripting capabilities.

Brokerage Platform Choice: The selection of a brokerage firm is a strategic decision. For active traders and those implementing algorithmic strategies, platforms offering advanced charting, swift order execution, comprehensive market data, and API access are paramount. Firms like Interactive Brokers are frequently favored due to their global reach, wide array of tradable instruments, and sophisticated trading tools suitable for quantitative analysis. Their Trader Workstation (TWS) platform, for instance, allows for complex order entry and risk analysis.

Data Management: Accurate and timely data is the fuel for any quantitative model. This includes real-time prices for the underlying asset, option chains, historical price data for backtesting, interest rates, and crucially, implied volatility data. Many brokers provide this data, but for more demanding applications, specialized data vendors might be necessary. Ensuring data cleanliness and integrity is an ongoing task.

Software and Scripting: While spreadsheets can be used for basic Black-Scholes calculations, professional quantitative trading often necessitates more advanced tools. Python, with libraries such as NumPy, Pandas, and SciPy, has become an industry standard for financial modeling, data analysis, and algorithmic trading. The availability of pre-written code, like the example found on GitHub, significantly lowers the barrier to entry for those looking to automate their trading strategies. This allows for rapid testing of hypotheses and the development of complex, rule-based trading systems that can execute trades automatically based on market conditions and model outputs.

Integration and Automation: The ultimate goal for many quantitative traders is to automate their strategies. This involves integrating the pricing model with the brokerage's API to place orders automatically when predefined conditions are met. This not only enhances efficiency but also removes the emotional component from trading decisions, leading to more disciplined execution. Such automation requires a solid understanding of programming and financial markets, underscoring the value of resources like Quant Guild for developing these advanced skill sets.

The synergy between a powerful brokerage, reliable data, and flexible software tools is what transforms the theoretical framework of the Black-Scholes model into a potent, profit-generating trading machine. Investing in the right technological infrastructure is a critical step for any trader serious about competing in today's markets.

Strategist's Verdict: Is Black-Scholes Your Next Profit Center?

The Black-Scholes model is more than an academic exercise; it's a potent tool for profit if wielded with precision and discipline. Its strength lies in providing a standardized, quantitative approach to option valuation, allowing traders to identify potential mispricings and exploit market inefficiencies. The critical inputs – stock price, strike price, time to expiration, risk-free rate, and volatility – are the levers you can pull to understand and predict option premiums.

Opportunity Assessment: The primary opportunity arises from discrepancies between the model's theoretical price and the actual market price of an option. By systematically calculating these theoretical values and comparing them with market quotes, disciplined traders can uncover potential arbitrage or strategic entry points. Furthermore, the model's sensitivity to implied volatility offers a direct pathway to strategies that capitalize on changes in market expectations regarding future price swings.

Risk/Reward Profile: The effectiveness of Black-Scholes is intrinsically linked to risk management. The leverage inherent in options means that while potential profits can be substantial, losses can also be significant. Mastering the 'Greeks' (Delta, Gamma, Theta, Vega) is non-negotiable. These metrics allow for precise risk assessment and hedging, enabling traders to construct portfolios that align with their risk tolerance and profit objectives. Without a robust risk management protocol, even the most sophisticated quantitative models can lead to catastrophic losses.

Actionability for the Trader: For the aspiring quantitative trader, implementing the Black-Scholes model requires a commitment to learning and adopting the right tools. This involves understanding the mathematics, setting up reliable data feeds, and choosing appropriate software – be it sophisticated spreadsheets, Python scripting, or integrated brokerage platforms. Resources like Quant Guild and their associated coding repositories provide invaluable practical guidance for this implementation phase.

Verdict: The Black-Scholes model is not a magic bullet, but it is a foundational pillar for sophisticated options trading. Its continued relevance in hedge funds and proprietary trading desks attests to its power. For traders willing to put in the work – mastering its inputs, understanding its limitations, diligently managing risk, and leveraging the right technology – it represents a significant opportunity to gain a quantifiable edge and potentially unlock new profit centers. The key is rigorous analysis, disciplined execution, and continuous adaptation to market dynamics.

Questions Fréquentes

Q: What is the Black-Scholes model used for?

A: The Black-Scholes model is primarily used to calculate the theoretical price of European-style options. It provides a framework for understanding option pricing based on several key variables.

Q: What are the key inputs for the Black-Scholes model?

A: The model requires the current stock price, the option's strike price, time to expiration, the risk-free interest rate, and the expected volatility of the underlying asset.

Q: Can the Black-Scholes model be used for American options?

A: The standard Black-Scholes model is designed for European options, which can only be exercised at expiration. While adaptations exist, it doesn't inherently account for the early exercise feature of American options.

Q: How can I start trading options using the Black-Scholes model?

A: To begin, you need a solid understanding of options, the Black-Scholes inputs, and access to a trading platform. Practical implementation often involves using financial software or coding your own models, as detailed in this guide.

Your Mission: Implement Your First Black-Scholes Calculation

Now that you understand the framework and practical steps involved in using the Black-Scholes model, it's time to put your knowledge into action. The true mastery of any financial model comes from hands-on application.

Your Challenge: For the next 48 hours, identify a publicly traded European-style option (e.g., on the S&P 500 E-mini futures or a major stock with liquid options). Gather the necessary inputs: current underlying price, strike price, time to expiration (in years), a current risk-free rate (e.g., a US Treasury yield), and an estimate for implied volatility. Use a readily available online calculator, a spreadsheet template, or the provided Jupyter Notebook to calculate its theoretical Black-Scholes price. Compare this theoretical price to its current market price. Note down any significant difference and hypothesize why that discrepancy might exist.

Share your findings and your hypothesis in the comments below. Did you find a potential mispricing? What factors do you think contributed to it? Your active participation is crucial for cementing this knowledge and developing the sharp analytical skills required for profitable trading.

About The Author

The Financial Strategist is a seasoned business consultant and market analyst with over a decade of experience guiding entrepreneurs and investors toward maximizing their profitability. Their methodology is grounded in rigorous data analysis, systematic approach, and an unwavering commitment to execution excellence. They specialize in deconstructing complex financial models and business strategies into actionable plans, empowering individuals to achieve their financial goals.

No hay comentarios:

Publicar un comentario